print("=" * 60)

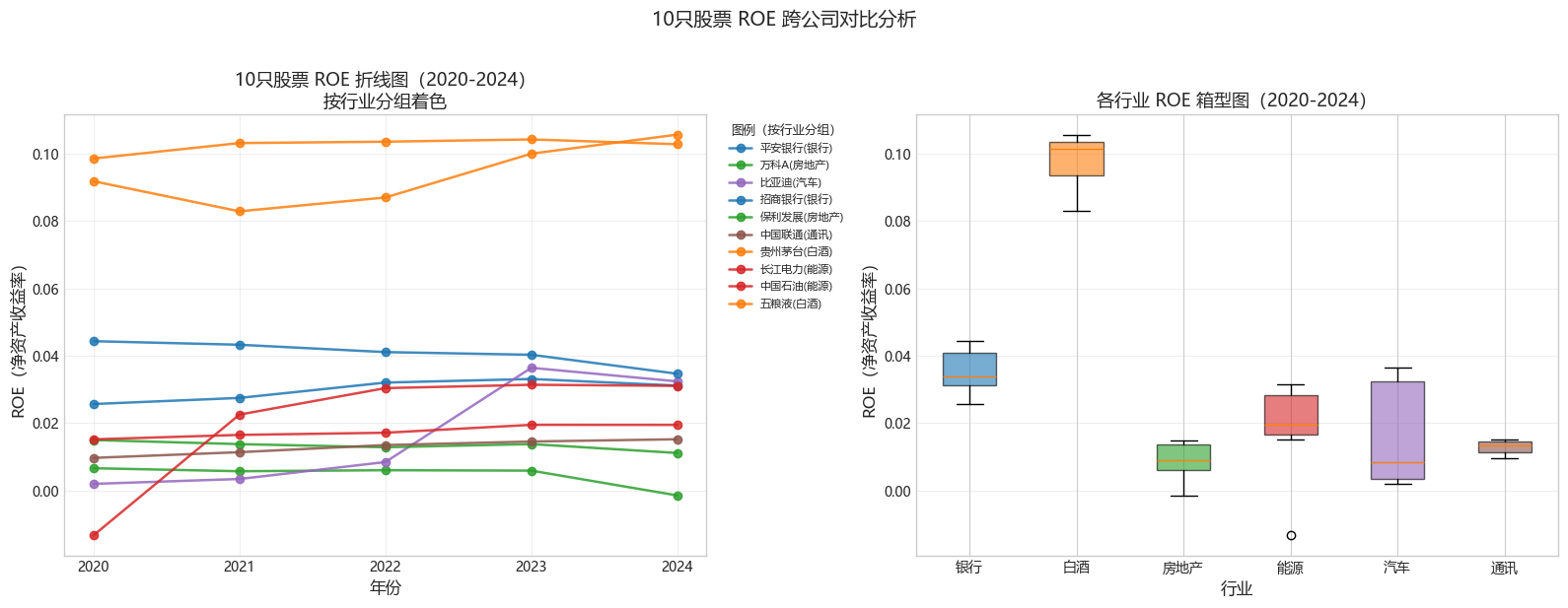

print("图5:ROE 跨公司对比")

print("=" * 60)

fin = pd.read_csv(f"{project_root}/data/finance/finance_ratios.csv")

roe = fin[(fin['indicator'] == 'roeAvg') & (fin['year'] <= 2024)].copy()

roe['year'] = roe['year'].astype(str)

roe['code'] = roe['code'].apply(lambda x: str(int(x)))

stripped_to_name = {str(int(s["code"])): s["name"] for s in stock_list}

stripped_to_industry = {str(int(s["code"])): s["industry"] for s in stock_list}

roe = roe[roe['code'].isin(stripped_to_name.keys())]

roe_pivot = roe.pivot_table(index='code', columns='year', values='value')

roe_pivot = roe_pivot.sort_index()

print(f"ROE数据范围: {roe['year'].min()} - {roe['year'].max()}")

print(f"股票数: {roe['code'].nunique()}")

print("\n各股票 ROE 均值(2020-2024):")

for idx in roe_pivot.index:

name = stripped_to_name.get(idx, idx)

print(f" {name}: {roe_pivot.loc[idx].mean():.4f}")

industry_colors_roe = {

'银行': '#1f77b4', '白酒': '#ff7f0e', '房地产': '#2ca02c',

'能源': '#d62728', '汽车': '#9467bd', '通讯': '#8c564b'

}

years = roe_pivot.columns.tolist()

fig, axes = plt.subplots(1, 2, figsize=(16, 6))

ax1 = axes[0]

for code_s in roe_pivot.index:

ind = stripped_to_industry.get(code_s, '其他')

name = stripped_to_name.get(code_s, code_s)

ax1.plot(years, roe_pivot.loc[code_s].values,

marker='o', markersize=6,

label=f"{name}({ind})",

color=industry_colors_roe.get(ind, 'gray'), linewidth=1.8, alpha=0.85)

ax1.set_xlabel('年份', fontsize=12)

ax1.set_ylabel('ROE(净资产收益率)', fontsize=12)

ax1.set_title('10只股票 ROE 折线图(2020-2024)\n按行业分组着色', fontsize=13)

ax1.legend(bbox_to_anchor=(1.02, 1), loc='upper left', fontsize=8, title='图例(按行业分组)', title_fontsize=9)

ax1.set_xticks(years)

ax1.grid(True, alpha=0.3)

ax2 = axes[1]

ind_data, ind_labels, ind_colors = [], [], []

for ind in ['银行', '白酒', '房地产', '能源', '汽车', '通讯']:

codes_s = [str(int(s['code'])) for s in stock_list if s['industry'] == ind]

valid = [c for c in codes_s if c in roe_pivot.index]

if not valid:

continue

vals = roe_pivot.loc[valid].values.flatten()

vals = vals[~np.isnan(vals)]

ind_data.append(vals)

ind_labels.append(ind)

ind_colors.append(industry_colors_roe.get(ind, 'gray'))

bp = ax2.boxplot(ind_data, labels=ind_labels, patch_artist=True, notch=False)

for patch, color in zip(bp['boxes'], ind_colors):

patch.set_facecolor(color)

patch.set_alpha(0.6)

ax2.set_xlabel('行业', fontsize=12)

ax2.set_ylabel('ROE(净资产收益率)', fontsize=12)

ax2.set_title('各行业 ROE 箱型图(2020-2024)', fontsize=13)

ax2.grid(True, alpha=0.3, axis='y')

plt.suptitle('10只股票 ROE 跨公司对比分析', fontsize=14, y=1.02)

plt.tight_layout()

plt.savefig(f"{project_root}/output/fig5_roe_comparison.png", dpi=150, bbox_inches='tight')

plt.show()

print("\n图5(ROE对比)已保存至 output/fig5_roe_comparison.png")